Comparing export-oriented industrial policies: 21st century China and 20th century Japan

Essay/working notes

Context

The meteoric rise of China in the late 20th century is characterized by supplying all sorts of goods to the global consumer market at competitively cheap prices, cementing its status as the world’s “gigantic manufacturing export machine” (Kroeber). However, weakening domestic demand, exacerbated by the recent tariff shock imposed by the United States, reveals the Chinese economy whose health is over-dependent on supplying for global markets.

I thought of comparing the direction of post-WWII Japan and China’s industrial policy. Both pursued state-driven EOI strategy for development, both ran their country as a manufacturing powerhouse – having once been or is currently deemed as the “second largest economy” in the world, they both faced intense protectionist rhetoric from the U.S during their respective heights. Both arguably running their economy on three-legged stool – businessmen, politicians, bureaucrats. Both relied on industrial policy to counter slumps, doubling down on R&D and manufacturing expansion.

The question: Given these overarching similarities, will adopting elements of the Japanese ‘miracle’ growth machine work within a Chinese context?

Understanding China from a glance

The main contextual understanding is that China is running an enormous trade surplus with the rest of the global economy by pursuing an industrial policy where they did not focus on exporting a few particular goods, but rather went all-in on producing all kinds of goods – homeware, clothing. Their manufacturing dominance is so strong that whatever you can think of – the items you’re using right now – are probably Made in China. It brought light to the fact that domestic consumption as a component of the total economy is tiny, so very little local demand for goods and services. That’s why it’s deemed as the world’s “gigantic manufacturing export machine.” The problem that lies here is that, as of current, since domestic demand accounts for such a miniscule portion of the immense output of produced goods, decreased demand of Chinese goods from trading partners (e.g. imposing tariffs) would decimate the operations of many industries that lie on the backs.

In a nutshell, Japanese industrial policy selected key industries as “pillars” to focus research and development on centrally directing funding and preferential market opportunities for firms to invest R&D in specific industries. MITI guided investment in specific industries, macro planning, credit lending and market preference / monopolies. Focused on heavy industry, ships, machinery, cars, and household durable goods (appliances, furniture, and electronics). Global scale objective despite few resources. Products of this developmental model were the large scale oligarchies in Japan, known as zaibatsu (Mitsui, Mitsubishi, Sumitomo).

On the other hand, China was successful in industrial policy not because they picked the right industries, rather because they were “adept at building the right enabling structure.” State-owned enterprises delivered essential services and heavy industry, whereas private enterprises were allowed to flourish and go on their own path. To introduce private enterprise production, China set up special economic zones (SEZ). In this system, the central authority held municipalities accountable for their economic growth and losses, creating a system within the local level to encourage competition and innovation. (Characteristics include: low overheads, low taxes, low labour cost, foreign investor JVs, and global free market access in the SEZs.)

In essence, Chinese leadership didn’t have a pre-ordained view of what to produce, but it knew it had to pursue an export-oriented strategy for western markets. Enabling all-purpose technology right from the start and then scale them up, then a lot of good things can happen as a result of that, regardless of how effective you are at picking winners sector by sector in industrial policy.” Gamut of goods (with underlying all-purpose technology system)

Jake Sullivan (Former National Security Advisor to President Biden): “The PRC is producing far more than domestic demand, dumping excess into global markets at artificially low prices, driving manufacturers around the world out of business, and creating a chokehold on supply chains.” Jake Sullivan posed the idea of “de-risking” rather than “decoupling,” indicating that supply chains for producing things that are crucial to the U.S. military defense (amongst others) should be ‘de-risked’ from geopolitical competitors like China.

Japan’s rise was facilitated greatly by the full support it had from the U.S. during the post-WWII period to develop their economy (with the U.S. taking a laissez-faire stance in what now seems like complacency), such that Japan greatly bolstered its manufacturing capacities in key industries, became the world’s manufacturing center for those industries, and ran a trade surplus up till the Plaza Accord in 1985 as the turning point. The Japanese economy boomed because of manufacturing contracts for the three key industries necessary for waging warfare: communications, automobiles, textile. The challenge that China is facing, in addition to weak domestic demand, is that its export-oriented model is experiencing increasing stress under protectionist measures from the U.S as an independent geopolitical competitor.

Could Chinese economic planning learn from Japanese policy planning?

Made in China 2025 – the strategic industrial policy document – laid the direction for industrial ambitions and set targets such as key performance indicators for local bureaucrats to strive for, all the while being very much less state-driven than post-WWII Japanese MITI central planning by leaving the implementation strategy up to localities. To quote from the paper: “But the plan offered limited guidance on implementation, leaving ample room for interpretation, duplication, and misalignment at the provincial and municipal levels. In this sense, MIC2025 was less a coordinated policy execution than a signaling device.”

Something Chinese economic planning could learn is fostering selected key industries for growth. Rather than producing a broad range of goods, the Japanese selected a few areas in which they could develop high-quality goods to produce in vast quantities at competitive prices. Fostering the R&D of successful players in these key industries like renewable energy and semiconductor industry will be crucial in their agenda to make the transition from running factories on ‘dirty’ energy (e.g. coal) to running it on ‘green’ energy, and to create a completely-domestic energy-grid supply to create complete energy self-reliance. In the same vein of thought, Chinese industrial planning could double down on this by making renewables – e.g. EVs – priority production.

It seems like deflationary pressures on an economy with ‘weak’ demand and a “persistent property crisis” (Li et al) are the driving factors behind declining profits in industrial sectors, which is in turn propelled by “insufficient effective demand.” Tariffs and the subsequent decline in demand abroad for Chinese-manufactured goods reveals the overproduction of exports, and how the determinant of the economy’s health is skewed towards international demand for exports. In this sense, simply pursuing an export-oriented economy won’t work – what would work is bolstering domestic demand and redirecting manufacturing capacities to key industries rather than running the whole course of goods production. How to do so remains to be discussed.

Differences to keep in mind:

China’s manufacturing base is larger and more globally integrated than Japan’s 1960s–80s economy; ties into talks of to what extent can the U.S. economy – and any economy – ‘derisk’ from Chinese goods.

Modern U.S.-China tech containment exceeds 1980s U.S.-Japan trade friction.

China’s consumption (53.4% of GDP) is weaker than Japan’s pre-1991 levels (63.3%).

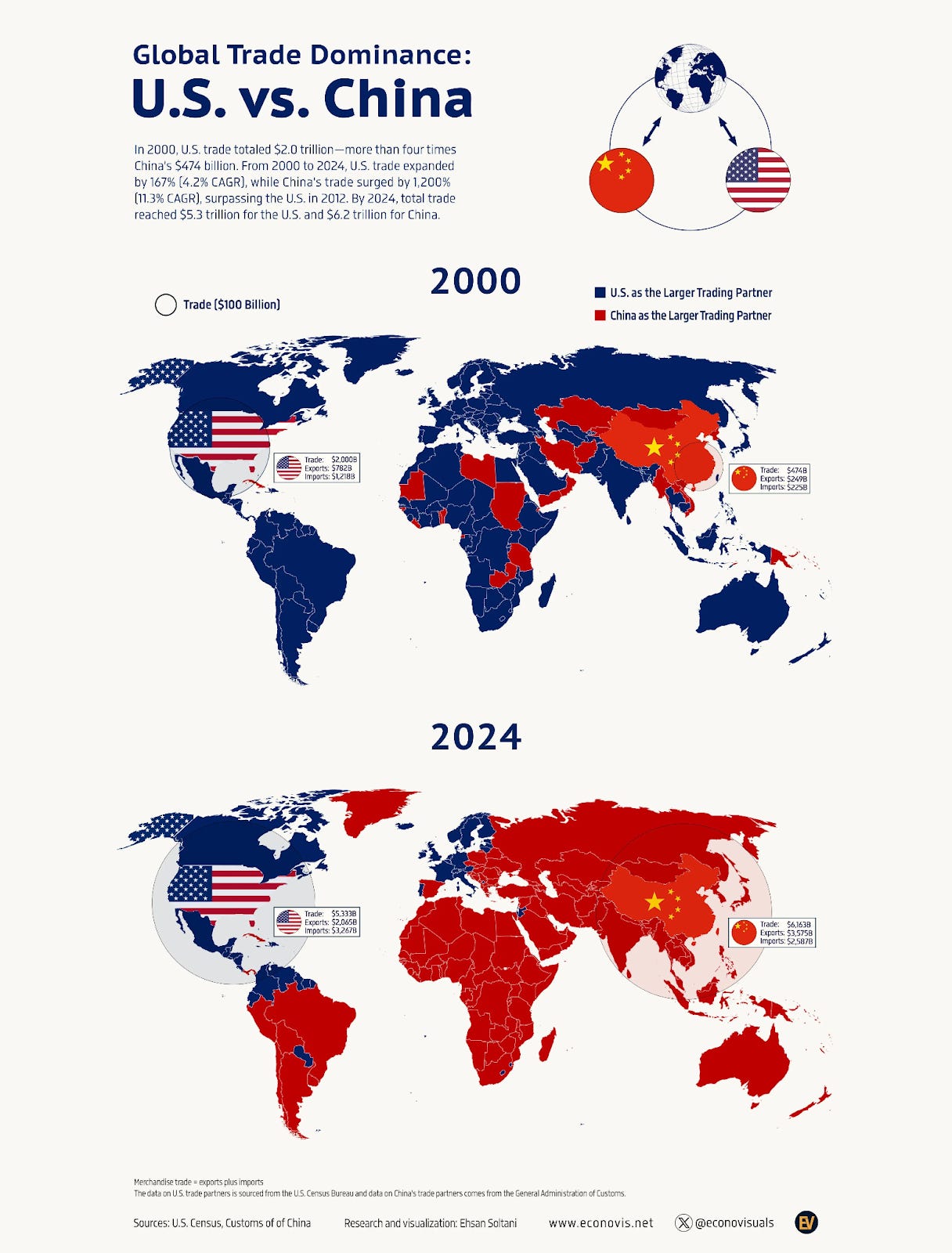

An infamous infographic: Who is the bigger trading partner — China or the U.S.? A visual comparison between 2000 and 2024.

Annotated bibliography

Kuo, Kaiser. “Made in China 2.0: The future of global manufacturing?” World Economic Forum, June 26, 2025. Accessed July 6, 2025. https://www.weforum.org/stories/2025/06/how-china-is-reinventing-the-future-of-global-manufacturing/.

Chinese industrial policy is focusing on powering itself on renewable energy and self-reliance. Industrial processes are marked by a transition from running factories on ‘dirty’ energy (e.g. coal) to running it on ‘green’ energy, such that energy-grid supply can become completely domestic to create complete energy self-reliance – aka. a renewable-powered domestic electricity grid.

Made in China 2025’s agenda was to move Chinese manufacturing up the value chain; from producing low-end mass consumer goods, to more high-tech goods such as semiconductors, robotics, aerospace, and medicine. It laid the direction for industrial ambitions and set targets such as key performance indicators for local bureaucrats to strive for, all the while being very much less state-driven than post-WWII Japanese MITI central planning by leaving the implementation strategy up to localities. To quote from the paper: “But the plan offered limited guidance on implementation, leaving ample room for interpretation, duplication, and misalignment at the provincial and municipal levels. In this sense, MIC2025 was less a coordinated policy execution than a signaling device”

Evaluation of MIC2025’s success:

Over 75% of global lithium-ion battery manufacturing

Nearly 80% of solar module production

The major producer of the world’s electric vehicles

High-speed rail a sign of engineering prowess

Robotics and sensor technologies nearing global leaders

By doing, you learn. The flywheel of innovation is the hands-on knowledge that develops in the hands of the makers, via the “tacit, experiential know-how that accumulates on factory floors, in supply chain coordination, and in the trial-and-error of prototyping.” Another defining characteristic is that to emerge as new innovators of technologies that don’t have an established leader or streamlined workflow (e.g. EVs) is that these companies are less so “legacy manufacturers” and more so motivated by “integrated systems thinking, technical fluency, and global competitiveness.”

McCormack, Alan. “Political economy of Australia’s engagement in the Asia Pacific region.” Zoom webinar, slide show, July 2025. https://drive.google.com/file/d/18VVIiPoyJh-7ryeoLqvmVGFClFuRjVGS/view?usp=sharing.

Both Chinese and post-WWII ‘80s Japanese industrial policy are very state-driven, with centrally-planned state objectives powering industry R&D.

Japanese industrial policy focused on centrally directing funding and preferential market opportunities for firms to invest R&D in specific industries that the state set its targets on. Japan’s MITI led macro planning, credit lending and market preference / monopolies. Focused on heavy industry, ships, machinery, cars, and household durable goods (appliances, furniture, and electronics). Global scale objective despite few resources. Products of this developmental model were the large scale oligarchies in Japan, known as zaibatsu (Mitsui, Mitsubishi, Sumitomo). The economic system can be likened to a three-legged machine of businessmen-politicans-bureaucrats powering Japan, Inc.

In Chinese industrial policy, state-owned enterprises delivered essential services and heavy industry. To introduce private enterprise production, China set up special economic zones (SEZ). In this system, the central authority held municipalities accountable for their economic growth and losses, creating a competitive system within the municipal officers to maximize the treadmill of development. Characteristics include: low overheads, low taxes, low labour cost, foreign investor JVs, and global free market access in the SEZs.

Kroeber, Arthur. “China’s Manufacturing Dominance: State Directives & Ruthless Competition — Arthur Kroeber.” Interview by Dwarkesh Patel, June 19, 2025. Accessed June 30, 2025. https://www.dwarkesh.com/p/arthur-kroeber.

The main contextual understanding is that China is running an enormous trade surplus with the rest of the global economy by pursuing an industrial policy where they did not focus on exporting a few particular goods, but rather went all-in on producing all kinds of goods – homeware, clothing. Their manufacturing dominance is so strong that whatever you can think of – the items you’re using right now – are probably Made in China. It brought light to the fact that domestic consumption as a component of the total economy is tiny, so very little local demand for goods and services. That’s why it’s deemed as the world’s “gigantic manufacturing export machine.” The problem that lies here is that, as of current, since domestic demand accounts for such a miniscule portion of the immense output of produced goods, decreased demand of Chinese goods from trading partners (e.g. imposing tariffs) would decimate the operations of many industries that lie on the backs.

Although Japan and China are both East Asian countries with state-driven economies, their geopolitical situations couldn’t be more different. China is an independent geo-political actor situated in a dangerous neighborhood, with fourteen neighbors and four nuclear-armed. One might ask what does geopolitical independence have to do with economic decision-making. Japan’s rise was facilitated greatly by the full support it had from the U.S. during the post-WWII period to develop their economy (with the U.S. taking a laissez-faire stance in what now seems like complacency), such that Japan greatly bolstered its manufacturing capacities in key industries, became the world’s manufacturing center for those industries, and ran a trade surplus up till the Plaza Accord in 1985 as the turning point. Even towards their geopolitical ally, the attitude in Washington towards Japanese manufacturing was quite negative. China’s challenge is that in addition to weak domestic demand, its export-oriented model is experiencing increasing stress under protectionist measures from the U.S as an independent geopolitical competitor.

Kroeber makes the remark that China was successful in industrial policy not because they picked the right industries, rather because they were “adept at building the right enabling structure.” Chinese leadership didn’t have a pre-ordained view of what to produce, but it knew it had to pursue an export-oriented strategy for western markets. Kroeber points to two things: informatization and electrification. In his own words: Get a few of “enabling all-purpose technology decisions right earlier and then scale them up, then a lot of good things can happen as a result of that, regardless of how effective you are at picking winners sector by sector in industrial policy.”

Two questions:

“How do you integrate China’s growing power, wealth, industrial might into the world in a way that societies around the world can tolerate? There has to be an agreed set of rules about how it interacts with the rest of the world, so that everyone feels that they are benefiting. We don’t really have that agreement right now.”

In light of how China currently houses the manufacturing power to produce the vast majority of the world’s low-cost goods, how can large countries maintain a diversified production structure? Cf. Kroeber - “If you lose the capacity to run a manufacturing economy that employs large amounts of people, there’s a lot of disruptions that come along with that. (In the purely financialized economy we had in the early 2000s as a result of this bargain with China wound up to be pretty bad for the social impact.)”

Jake Sullivan (Former National Security Advisor to President Biden): “The PRC is producing far more than domestic demand, dumping excess into global markets at artificially low prices, driving manufacturers around the world out of business, and creating a chokehold on supply chains.” Jake Sullivan posed the idea of “de-risking” rather than “decoupling,” indicating that supply chains for producing things that are crucial to the U.S. military defense (amongst others) should be ‘de-risked’ from geopolitical competitors like China. Note that Japan was considered a geopolitical ally-asset, and in fact we learned that the Japanese economy boomed (especially three key industries necessary for waging warfare, namely communications, automobiles, textile) because of manufacturing contracts ordered by the U.S. for their wars in SEAsia – the Korean War, Vietnam War. Derisking may be viable for certain industries, but not all – and Chinese manufacturing runs the whole gamut.

Li, Qiaoyi, Tina Qiao, and Ryan Woo. “China’s May industrial profits slip back into sharp decline.” Reuters, June 27, 2025. https://www.reuters.com/business/autos-transportation/chinas-industrial-profits-slip-back-into-sharp-decline-may-2025-06-27/.

In a situation where industrial profits declined by 9.1% (Reuters) and manufacturing activity continues to contract for the third consecutive month (Bao), China’s manufacturing overcapacity and falling prices, exacerbated by U.S. tariffs, means that factories are under “immense strain” to maintain profit or break even – especially in exceptionally competitive industries like the automotive industry.

“Deflationary pressures” and a “persistent property crisis” are driving factors behind declining profits in industrial sectors, which is in turn propelled by “insufficient effective demand” – alluding to how tariffs and the subsequent decline in demand abroad for Chinese-manufactured goods reveals the overproduction of exports, and how the economy’s health is skewed towards demand for exports abroad. In fact, during the first five months of 2025, while profits in privately-owned enterprises rose slightly, profits in state-owned enterprises dropped by 7.4%.

Statistics summarizing changes in profit margins, in. May 2025

Profits at industrial firms: 9.1% decrease in May 2025 vs. May 2024

Profits at industrial firms: 1.1% decrease (first five months) vs. 2024

Profits at state-owned firms: 7.4% decrease (first five months) vs. 2024

Profits at private-sector firms: 0.3% increase (first five months) vs. 2024

Profits at foreign firms: 3.4% increase (first five months) vs. 2024

Frankel, Jeffrey. “The Plaza Accord, 30 Years Later.” National Bureau of Economic Research, December 2015. https://doi.org/10.3386/w21813.

Reading this working paper to understand what kind of a trade imbalance did Japan run with the U.S. prior to the Plaza Accord that definitively shifted the balance. Note “In the two years 1985-87, the dollar came back down 40 per cent. After the exchange rate turned around, so did the trade balance (with the usual lag). In the end, the US Congress refrained from enacting protectionist trade barriers.” Especially pertinent because the U.S. currently runs a significant trade deficit with China, meaning it imports far more than exports, with the trade deficit being a major resource of tension between the two countries and resulting in protectionist measures - like tariffs.

Quality is an important issue. Compared with China, Japan specialized in fewer areas but they produced high quality products. Still, their output is quite diverse. In the 1980's I bought a classical guitar made by Yamaha, who also makes vehicles. In the west, we don't really have companies like that that make really diverse products. The guitar was really good quality but also reasonably priced - so it beats Chinese products on quality and western products on price. And then China, like you said, they just make everything, and because they can do it a lot more cheaply, they flood western markets, but that may be changing now. It's also unsustainable because, as the standard of living rises in China, they won't be able to make products so cheaply. Interestingly, Australia has just signed a deal to buy some naval ships from Japan.